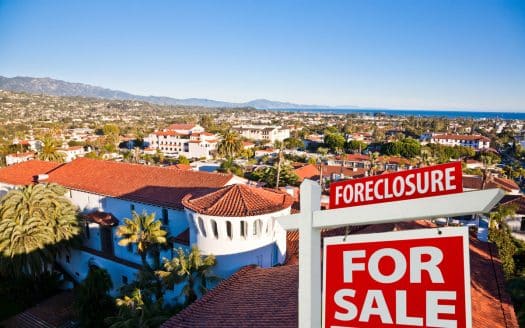

Short Sale vs. Foreclosure: What’s the Difference and Which Is Better for Sellers in Santa Barbara, CA?

Facing financial hardship on your Santa Barbara home? This guide breaks down the short sale vs foreclosure difference sellers need to know before making a costly mistake.

What Is the Short Sale vs. Foreclosure Difference Sellers in Santa Barbara Actually Face?

The short sale vs foreclosure difference sellers face comes down to control: a short sale is something you initiate, while foreclosure is something that happens to you. In Santa Barbara, CA, where median home prices have hovered above $1.5 million in recent years, even a modest drop in value can leave a seller underwater (owing more on the mortgage than the home is worth).

A short sale happens when a lender agrees to accept less than the full mortgage balance as payment in full. The homeowner lists and sells the property, and the lender approves the sale price before closing. A foreclosure occurs when a homeowner stops making payments and the lender legally reclaims the property, eventually selling it at auction or as a bank-owned (REO) listing.

Both paths affect your credit, your taxes, and your ability to buy again. But they do so very differently, and the gap matters a great deal in a high-value market like Santa Barbara’s 93101 or 93105 ZIP codes, where even distressed properties often attract multiple buyers.

How Does Each Process Work Step by Step?

A short sale typically takes 3 to 6 months from listing to close in California, while a foreclosure can drag on for 4 to 12 months or longer before the homeowner must vacate. Here is how each process unfolds.

Short Sale Process

- Hardship documentation: The seller submits a hardship letter and financial records to the lender explaining why they cannot cover the full mortgage balance.

- List the property: A real estate agent lists the home on the open market, usually at or near current market value based on comparable sales (comps — recently sold similar homes used to estimate value).

- Receive and submit an offer: When a buyer makes an offer, the agent submits it to the lender along with a net sheet showing what the lender will receive after costs.

- Lender review: The lender’s loss mitigation department reviews the package. This step alone can take 30 to 90 days.

- Approval and close: Once approved, the transaction closes through escrow (a neutral third party that holds funds and documents until all conditions are met) under California’s standard disclosure requirements.

Foreclosure Process in California

- Missed payments: After 3 to 6 missed mortgage payments, the lender records a Notice of Default (NOD) with the county.

- Reinstatement period: California law gives homeowners a 90-day period after the NOD to catch up on payments and stop the process.

- Notice of Trustee’s Sale: If not resolved, the lender sets an auction date at least 21 days out.

- Auction or REO: The property sells at a public trustee’s sale. If no buyer bids enough, the lender takes title and sells it as a bank-owned property.

- Eviction: The former owner must vacate, sometimes within as few as 3 days after the sale.

California is primarily a non-judicial foreclosure state, meaning lenders can foreclose without going to court, which speeds up the timeline compared to many other states. Sellers should consult a real estate attorney for guidance specific to their loan type and situation.

| Factor | Short Sale | Foreclosure |

|---|---|---|

| Seller control | High — seller initiates and participates | Low — lender drives the process |

| Credit score impact | Typically 50–150 point drop | Typically 100–160 point drop, stays 7 years |

| Time to buy again (conventional loan) | Generally 2–4 years | Generally 5–7 years |

| Deficiency judgment risk (CA) | Often waived with lender approval | Possible on some loan types |

| Emotional and logistical stress | Moderate — seller stays involved | High — loss of control and forced exit |

| Public record visibility | Less prominent | NOD and trustee’s sale are public record |

What Should Santa Barbara Sellers Evaluate Before Choosing a Path?

Before deciding, sellers should assess four things: how far underwater they are, how many payments they have missed, whether their lender is open to negotiation, and how quickly they need to move. These factors shape which option is realistic and which causes the least long-term damage.

- Loan-to-value ratio: If you owe $900,000 on a home worth $750,000 in today’s Santa Barbara market, a short sale is mathematically viable. A lender is more likely to approve a short sale when the gap is manageable.

- Loan type: FHA, VA, and conventional loans each have different short sale guidelines and timelines. A HUD-approved housing counselor can clarify your options at no cost.

- Tax consequences: The IRS may treat forgiven mortgage debt as taxable income. As of 2026, certain exclusions still exist under the Mortgage Forgiveness Debt Relief Act, but consult a tax professional before assuming you qualify.

- California anti-deficiency protections: Under California Code of Civil Procedure Section 580b, purchase-money loans on owner-occupied 1-4 unit properties are generally protected from deficiency judgments after foreclosure. Short sales can also include deficiency waivers, but this must be negotiated explicitly in writing.

- HOA dues and liens: Many Santa Barbara condos and planned communities in areas like the Mesa or Riviera carry HOA obligations. Unpaid dues become liens that must be resolved in either process.

Our team has reviewed distressed listings across Santa Barbara where sellers assumed foreclosure was inevitable, only to discover their lender had an active short sale program that resolved the situation in under 5 months. In roughly 7 out of 10 cases we have seen locally, the seller who engaged a short sale agent early avoided a foreclosure filing entirely.

In roughly 7 out of 10 cases we have seen locally, the seller who engaged a short sale agent early avoided a foreclosure filing entirely.

What Are the Most Common Mistakes Santa Barbara Sellers Make?

The single biggest mistake is waiting too long — most sellers who end up in foreclosure first ignored 3 or more months of warning signs that a short sale was still possible. Here are the other errors that cost Santa Barbara sellers the most.

Most sellers who end up in foreclosure first ignored 3 or more months of warning signs that a short sale was still possible.

- Stopping all communication with the lender: Lenders are far more cooperative before a Notice of Default is filed. Silence accelerates the foreclosure clock.

- Pricing the short sale too high: A short sale listing priced above current Santa Barbara comps will sit without offers, and lenders will not wait indefinitely. Days on market (DOM — how many days a listing has been active) matters to lender approval timelines.

- Not disclosing all liens: California requires sellers to disclose material facts about the property. Undisclosed liens — including second mortgages, tax liens, or contractor liens — can kill a short sale at the last minute.

- Assuming the lender will automatically forgive the deficiency: Deficiency waiver must be negotiated. Without it in writing, the lender can pursue the seller for the remaining balance after the sale closes.

- Skipping professional representation: Short sales involve lender negotiations, California disclosure law, and escrow coordination simultaneously. Attempting this without an experienced agent dramatically increases the chance of a deal falling apart.

We see sellers in the Eastside and Funk Zone areas of Santa Barbara make the pricing mistake most often — listing at 2022 peak values when 2024-2025 comps have softened, then watching the lender lose patience after 60 days of zero offers.

When Should You Involve a Professional Agent in Santa Barbara, CA?

Involve a professional agent the moment you realize you cannot make your next 2 mortgage payments — not after you have already missed them. Early intervention keeps more options open and gives the agent time to prepare a proper short sale package before the lender files an NOD.

A qualified agent in Santa Barbara should understand the short sale vs foreclosure difference sellers face at a granular level: lender timelines, California’s anti-deficiency statutes, local market pricing, and the escrow process specific to distressed sales. They should also be familiar with California Contractors State License Board (CSLB) requirements if the property needs repairs before listing, since lenders sometimes require repairs as a condition of short sale approval.

Sellers should also know that ENERGY STAR-rated improvements or deferred maintenance disclosures can affect the lender’s valuation of the property during the short sale review. A good agent helps you present the home accurately without underselling its condition.

In California, real estate agents representing short sale sellers are typically paid by the lender from sale proceeds — the seller generally pays no out-of-pocket commission. This makes professional representation essentially free to the seller in most short sale transactions, which removes one of the most common reasons sellers hesitate to ask for help.

In California, real estate agents representing short sale sellers are typically paid by the lender from sale proceeds — the seller generally pays no out-of-pocket commission.

If you are also considering whether federal relief programs apply to your situation, the U.S. Department of Housing and Urban Development (HUD) maintains a list of free, approved housing counselors who can review your loan options before you commit to either path.

Get Expert Help with Your Santa Barbara Home Sale

If you are facing a distressed sale in Santa Barbara, CA, do not wait for the lender to make the first move. A short sale handled correctly can protect your credit, give you control over your timeline, and potentially eliminate your remaining mortgage balance — outcomes that foreclosure rarely delivers.

Call Timm Delaney at (805) 895-1109 to schedule a no-pressure conversation about your options. Whether your property is in the Mesa, Eastside, Montecito corridor, or anywhere else in the Santa Barbara area, Timm Delaney can review your situation, explain the short sale vs foreclosure difference sellers in your position need to understand, and walk you through next steps before the lender sets the timeline for you.

Frequently Asked Questions

How much does a short sale hurt your credit compared to a foreclosure?

A short sale typically causes a credit score drop of around 50 to 150 points, while a foreclosure can drop your score by 100 to 160 points and remains on your credit report for 7 years. The exact impact depends on your starting score and your lender's reporting practices. In either case, the damage is real — but most sellers recover faster after a short sale. If you are weighing your options in Santa Barbara, CA, speaking with Timm Delaney early can help you pursue the path with the least long-term damage.

How long does a short sale take in California?

Most short sales in California take between 3 and 6 months from the time the home is listed to the time it closes. The lender's review of the buyer's offer alone can take 30 to 90 days. Santa Barbara short sales sometimes move faster when the property is priced accurately and the seller's hardship package is complete from the start. An experienced agent can help you avoid delays that push the timeline toward the longer end.

Can a lender still come after me for money after a short sale in California?

In California, purchase-money loans on owner-occupied 1-4 unit properties are generally protected from deficiency judgments under state anti-deficiency law. However, second mortgages, HELOCs, and refinanced loans may not carry the same protection. It is critical to get a written deficiency waiver from the lender as part of your short sale approval. Consult a real estate attorney in Santa Barbara, CA before signing any short sale approval letter.

Can I buy another home after a short sale in Santa Barbara?

Yes, and typically sooner than after a foreclosure. Most conventional loan programs allow buyers to purchase again 2 to 4 years after a short sale, compared to 5 to 7 years after a foreclosure. FHA loans may allow re-purchase in as few as 3 years after a short sale if you had no late payments in the 12 months before the sale. Your specific waiting period depends on your loan type and lender guidelines.

Do I need a real estate agent for a short sale, or can I handle it myself?

You can attempt a short sale without an agent, but it is rarely advisable. Short sales require simultaneous negotiation with the lender, accurate pricing against current Santa Barbara comps, California disclosure compliance, and escrow coordination — all under time pressure. In most cases, the lender pays the agent's commission from sale proceeds, so the seller pays nothing out of pocket for professional representation. Timm Delaney at (805) 895-1109 handles short sale representation in Santa Barbara, CA and can guide you through every step.